The UK Government published the final version of the UK Border Target Operating Model on 29th August 2023.

The document lays out the United Kingdom’s post-Brexit border controls, to be implemented from January 2024.

Below are the key updates to our assessment of the earlier draft, which was published in April.

Key Points:

- The plans remain largely unchanged from the draft version (assessment below)

- The Government has delayed delivery of the plans by 3 months

- First checks on EU SPS products start in January 2024 (delayed from October 2023)

- Risk categories for EU products of animal origin are available here

- Risk categories for non-EU products of animal origin are available here

- Risk categories for plants are here

- Irish exports to the UK will face full controls at the UK border

- Northern Ireland can import freely from the Republic and export freely to the GB mainland

This plan will affect anyone importing goods to the UK – from the EU or elsewhere. Every business importing goods into the UK will need to adjust to new processes, particularly those importing food, plant or animal products.

UK businesses trading with Northern Ireland will fall under the new Windsor Framework, agreed between the EU and UK in March 2023. You can read our analysis here of the Windsor Framework.

UK Border Target Operating Model: A Summary

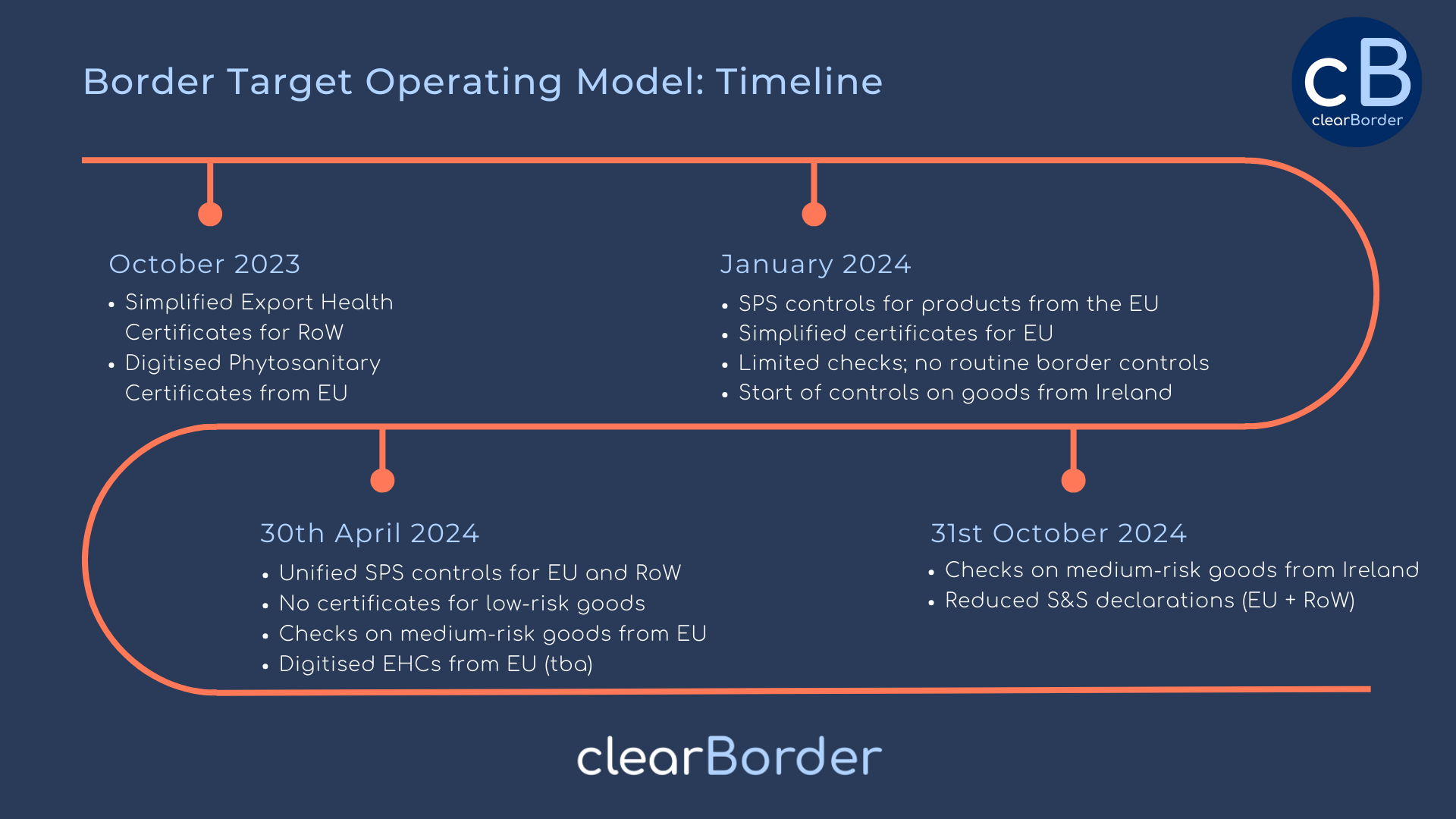

What’s happening to UK import controls and when?

Our timeline below summarises the changes:

- Simplified Health Certificates are being shared in 2023

- In January 2024 new requirements apply to imports from the EU

- In April 2024, EU and non-EU imports will be treated the same

- In October 2024, EU goods will face S&S controls

What is the UK Border Target Operating Model?

It’s a ‘targeting operating model’ for the UK border. In other words, a plan for the UK’s post-Brexit border controls.

What does it cover?

All goods – but particularly food, plant and animal products. There’s a bit about people too.

Who does it affect?

Anyone importing goods into the UK, particularly if you’re importing food, plant or animal products.

What does it mean?

It means the UK is ditching many border processes inherited from the EU. New processes will apply to food, animal and plant products from the EU. The same UK controls will apply to EU and RoW goods.

What’s changing?

- Sanitary and Phystosanitary (SPS) controls

- Safety and security (S&S or ‘entry summary’ ENS) declarations.

SPS controls

What are SPS controls? SPS controls are import rules applied to food, animal and plant products to protect the bio-security of the UK.

What’s changing for SPS controls? The UK is:

- Applying controls to EU imports (currently suspended since Brexit)

- Applying the same controls to EU and non-EU imports

- Developing risk categories for different SPS products

- Simplifying Export Health and Phystosanitary Certificates (EHCs and PCs)

- Developing ‘trusted trader’ schemes to further reduce SPS requirements

When? From January 2024.

Why? The UK has not applied SPS controls to imports from the EU since Brexit. The government aims to do two things: 1) to protect its border with the EU and 2) to simplify complicated processes it inherited from the EU.

What will this mean for businesses trading SPS goods?

- You’ll need to adjust to new processes from January 2024

- You should expect a new risk category and new certificates for your goods

- You should prepare for digitised processes with the Single Trade Window

- You should prepare for trusted trader schemes

Safety and Security Declarations

What are S&S (or ENS) declarations? S&S declarations inform border officials about the contents of individual consignments to check for security risks. The UK has suspended S&S declarations on EU imports since Brexit.

What’s changing for Safety and Security Declarations? The UK is:

- Simplifying S&S requirements from 37 data fields to 24

- Introducing S&S requirements for consignments shipped from the EU

- Planning automatic submissions in its future border platform (Single Trade Window)

When? In October 2024.

Why? The government hopes to have a single digital platform (‘Single Trade Window’) to automate a large part of the S&S requirement.

What will this mean for businesses trading goods?

- You’ll need to prepare for S&S declarations from October 2024

- Declarations will apply to all imports from the EU (and elsewhere)

- Hauliers or shippers will need to provide advanced information about consignments

- The government is hoping digital submissions will minimise the impact on traders

clearBorder’s View: Better Late than Never.

After years of delay and indecision, the UK appears finally to have settled on a policy for controlling imports through its border.

There’s much to recommend. The plans should simplify border processes, reduce bureaucracy and accelerate automation.

But for EU trade, these proposals will still feel like an additional burden: since leaving the EU, the UK has, essentially, left the border open.

Non-EU trade, however, will benefit from simplifications to health certificates and reduced processes for low risk goods.

EU and non-EU trade will be treated equally.

But the devil lies in the detail. The real opportunity will depend on whether the UK can achieve three things:

- Establish a flexible and dynamic approach to SPS risk categories. The proposed committee-based process risks becoming slow and murky. Effective risk management requires live data and transparency. The government should source and share risk data publicly.

- Simplify certificates but remove processes where they are not needed. The ‘Low Risk’ SPS category is a good example – these products will not require Export Health or Phytosanitary Certificates. The government should commit to an entirely digital process by the conclusion of the TOM implementation period.

- Generate meaningful benefits for ‘trusted traders’. The government proposes pilots to assess what additional assurance it can gain from trusted traders. They offer very little by way of benefits an SPS Trusted Trader scheme can offer business. Without benefits, businesses won’t join. We’ve published proposals here.

And of course the biggest requirement of all: to deliver a new scheme with an industry scarred by years of delay.

What should I do now?

If you import goods into the UK from the EU or anywhere else, you need to understand the UK Border Target Operating Model. You should

- Prepare for import controls if you import goods from the EU.

- Prepare for full customs and SPS controls on goods from the Republic of Ireland.

- Prepare for SPS controls if you import food, plants or animal products from the EU.

clearBorder are experts in import and export processes for international trade. We have a detailed understanding of existing processes and the UK government’s plans for border modernisation. Contact us for advice on the UK Border Target Operating Model and how we can help you prepare here.